Expedia- Making trip cancellation accessible for our travelers

Methods

Workshops

Competitive Analysis

User Research

Stakeholders

Senior Leadership

Developers

Insurance partners

Year

2022

Client

Expedia

Service

Commercial

Location

Gurgaon

Why?

Covid Chaos Cancelled: Designing Flexible Travel Booking

December 2021 saw travel bookings plummet by 30-50% due to Covid concerns, leaving many frustrated with inflexible policies and lost funds. This case study explores the design of a revolutionary travel booking platform that prioritizes flexibility and affordability. We tackled the challenge of empowering travelers to easily change or cancel trips while ensuring they maximize the value of their travel budget. Discover how we designed a user-centric solution for a post-pandemic world, prioritizing both freedom and financial security.

How?

Introducing a product that provides users with unparalleled flexibility.

In a world where plans could change in an instant, we introduced a product that gave travelers the ultimate flexibility to adapt their bookings with ease. Whether it was adjusting dates, destinations, or even canceling entirely, our feature ensured that users remained in control of their travel plans without the worry of rigid policies or unexpected fees. Designed to offer peace of mind and seamless changes, this product empowered users to travel on their terms, with freedom and confidence.

Research

A Travel Industry Catastrophe

2M

Bookings Cancelled

Reduced claim processing time (From 2 weeks to 3 days)

$500M

Revenue losses

CFAR specific revenue Generated in 2021-2022

103,000

Flights cancelled

Percentage of trips booked with CFAR that were subsequently canceled

77%

Less air travellers

From the pool of people who bought insurance

Secondary Research

Looking at what everyone’s doing

Top Competitor

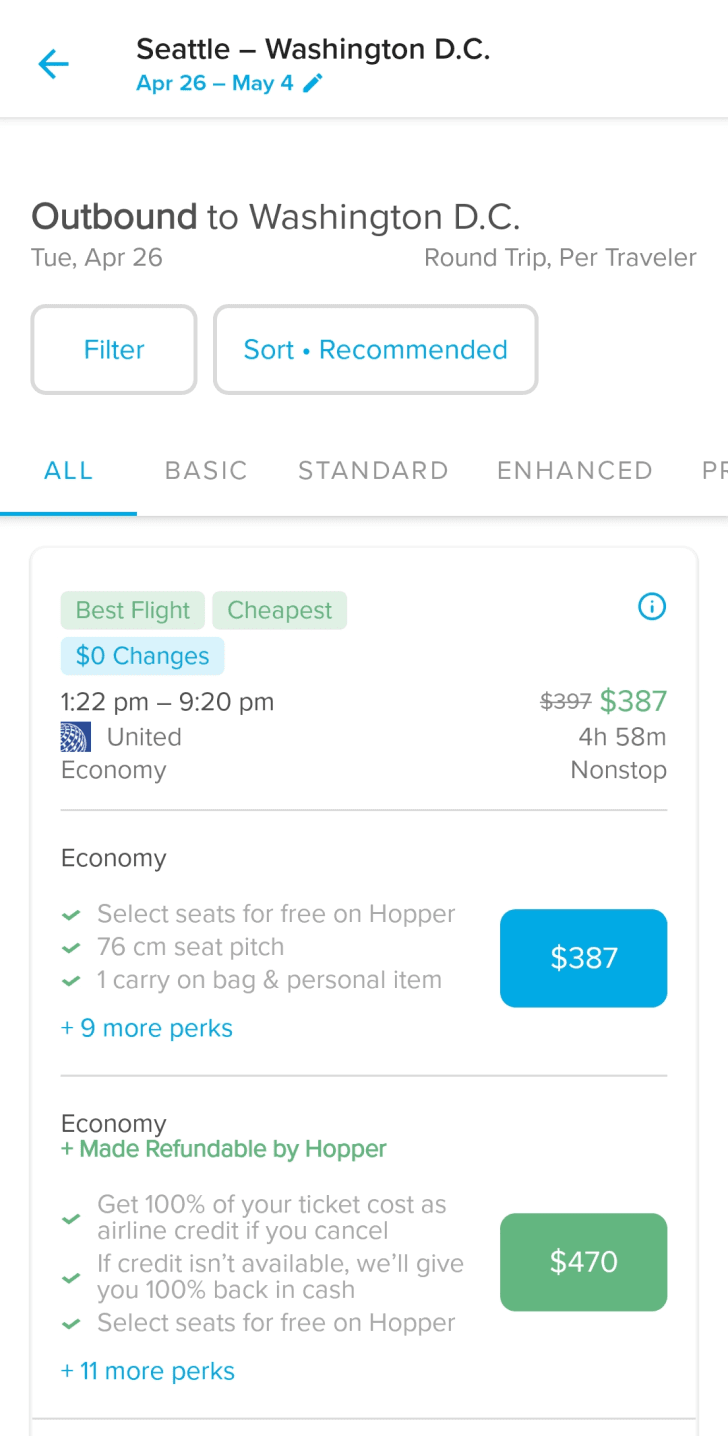

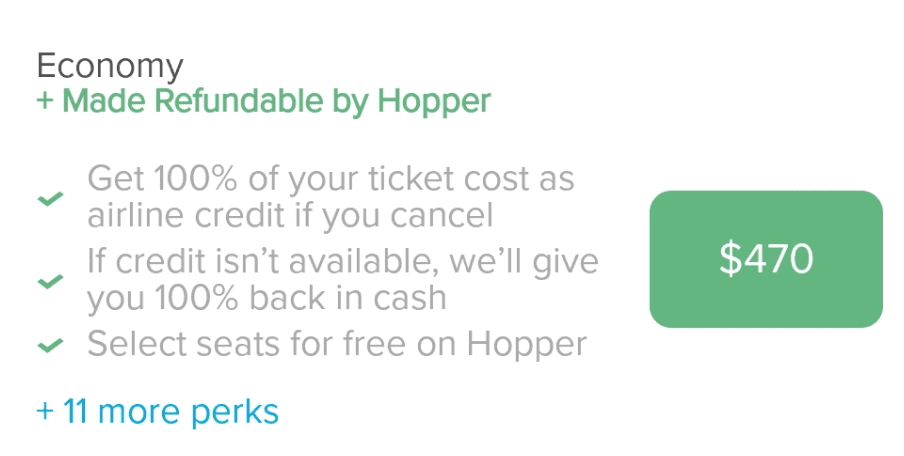

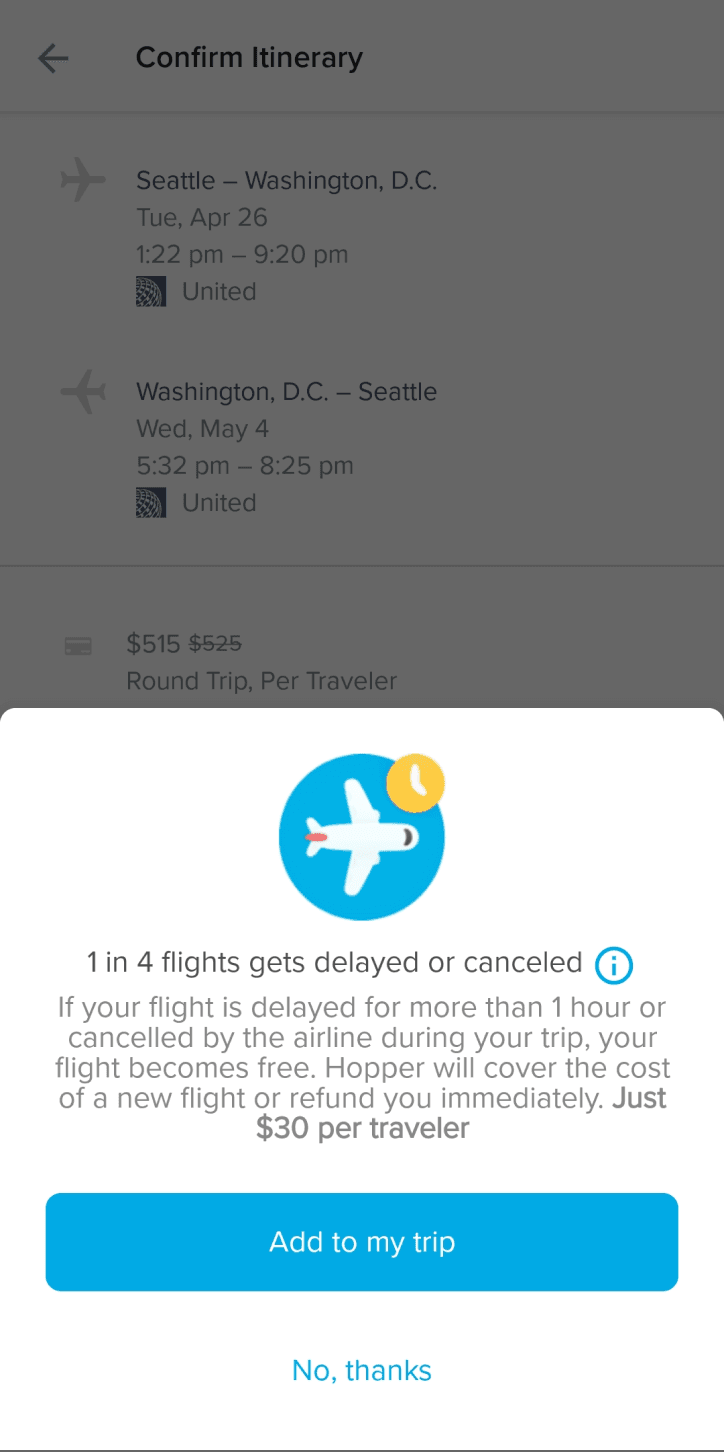

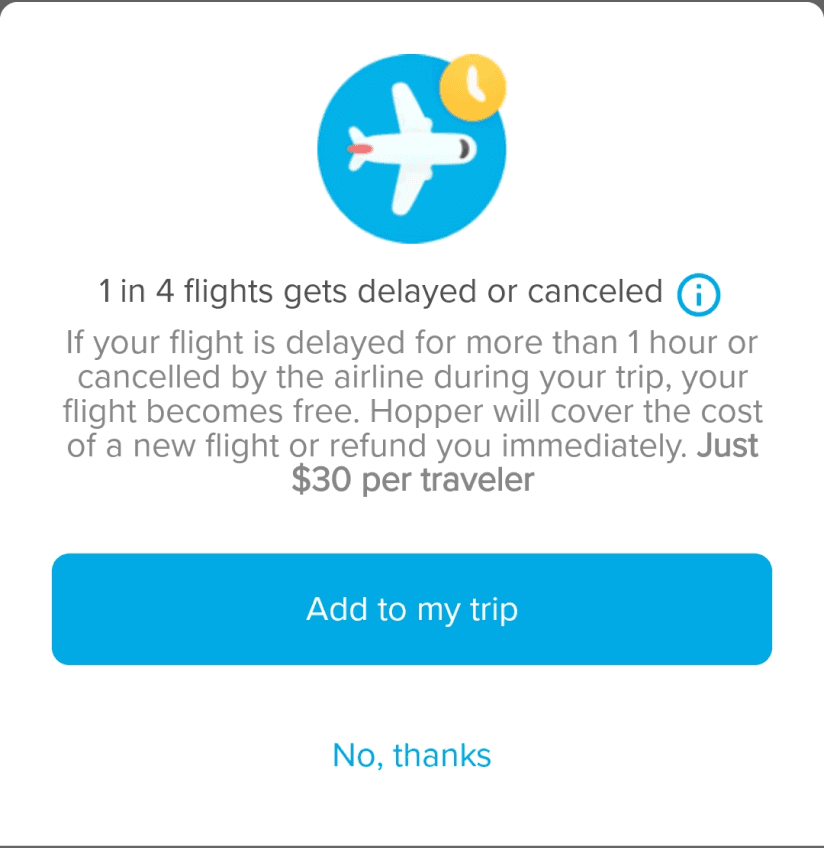

Hopper

Refunds:

100%: Select flights ("Made refundable by Hopper")

Flexible: "Cancel for Any Reason" & "Change for Any Reason" (both ways)

CFAR: 100/80% refund (roundtrip, applies to entire booking)

Refund Method: Airline credit (1 year) or cash

Method:

Airline credit (1 year) or cash

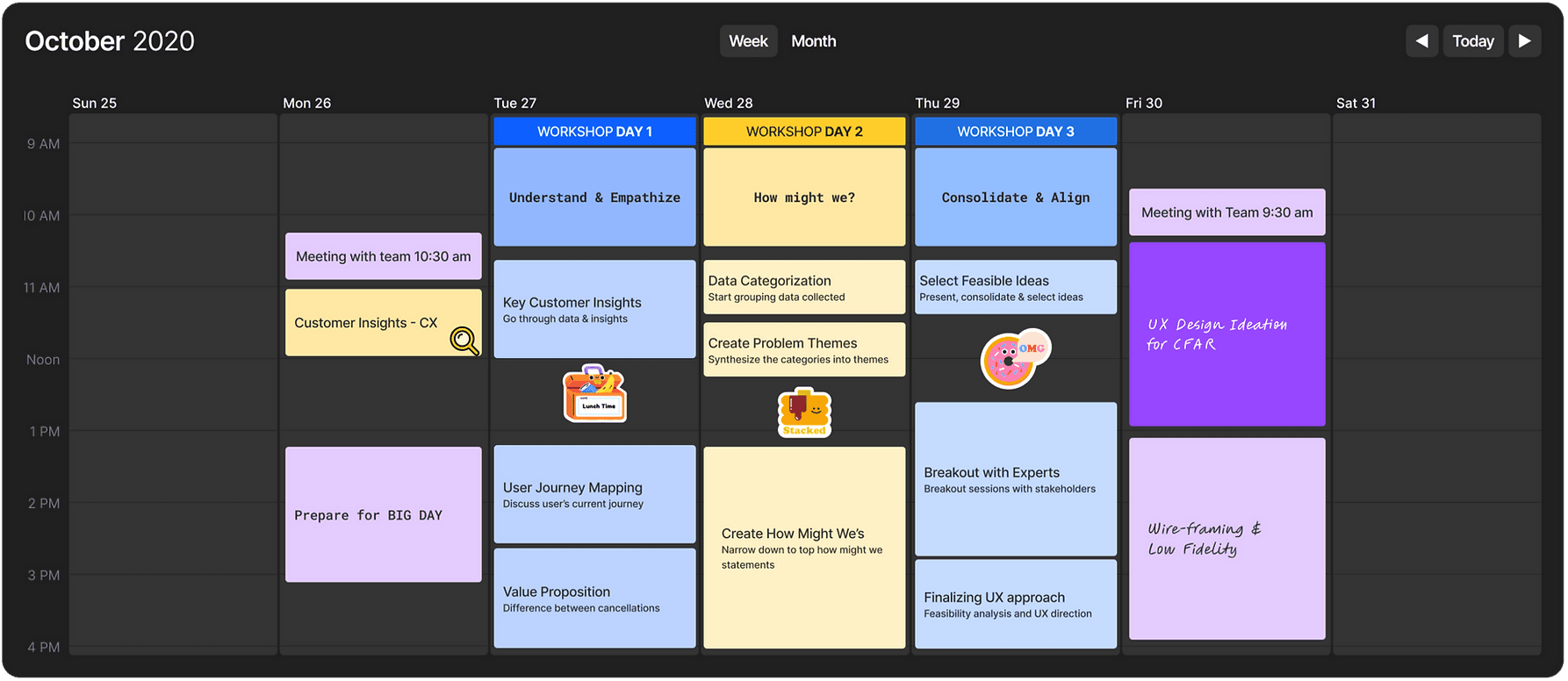

Research Workshop

Unite, Understand, Unfold

We conducted a three-day research workshop for the product stakeholders to come together, understand the user problems, reframe the problem statement into achievable How-Might-We's, and run a robust feasibility analysis with the experts to find the best UX approach.

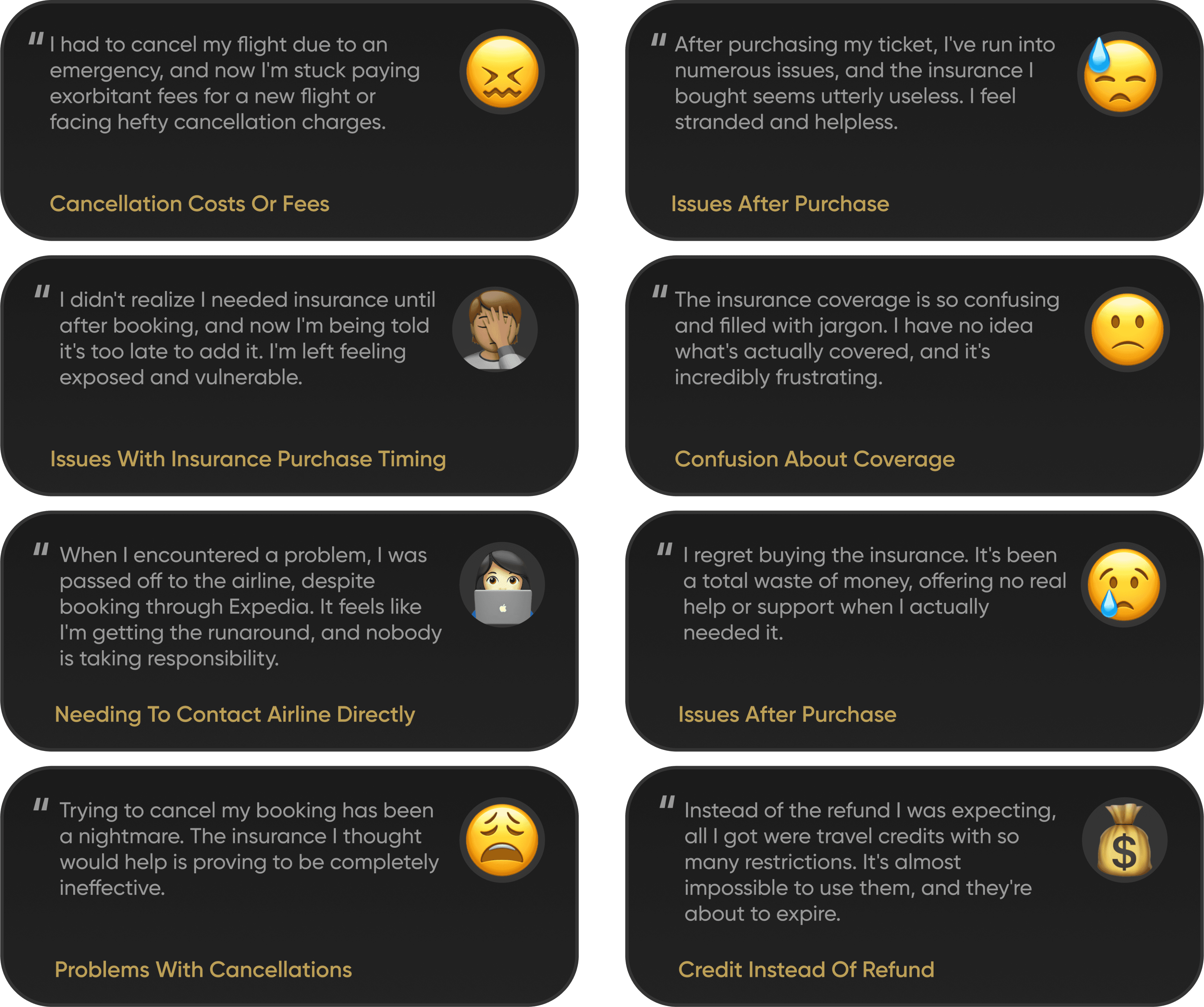

Customer Insights

Inflexible Bookings & Frustrated Travelers

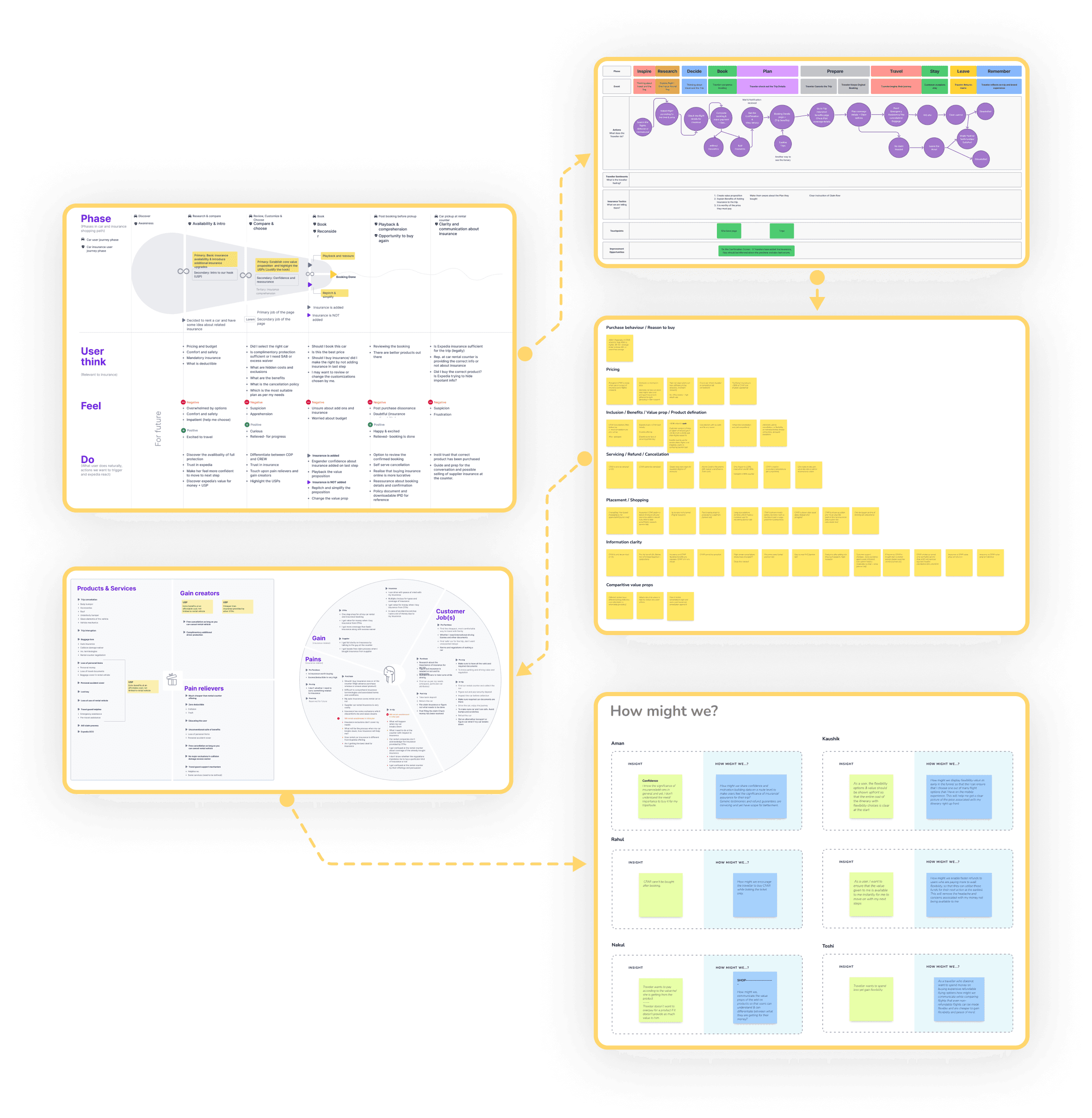

Research Workshop Process

A Collaborative Research Odyssey

The workshop included the following:

Defining User Journeys

Value Proposition Mapping

Grouping Insights

Value Proposition Canvas

How Might We

Design

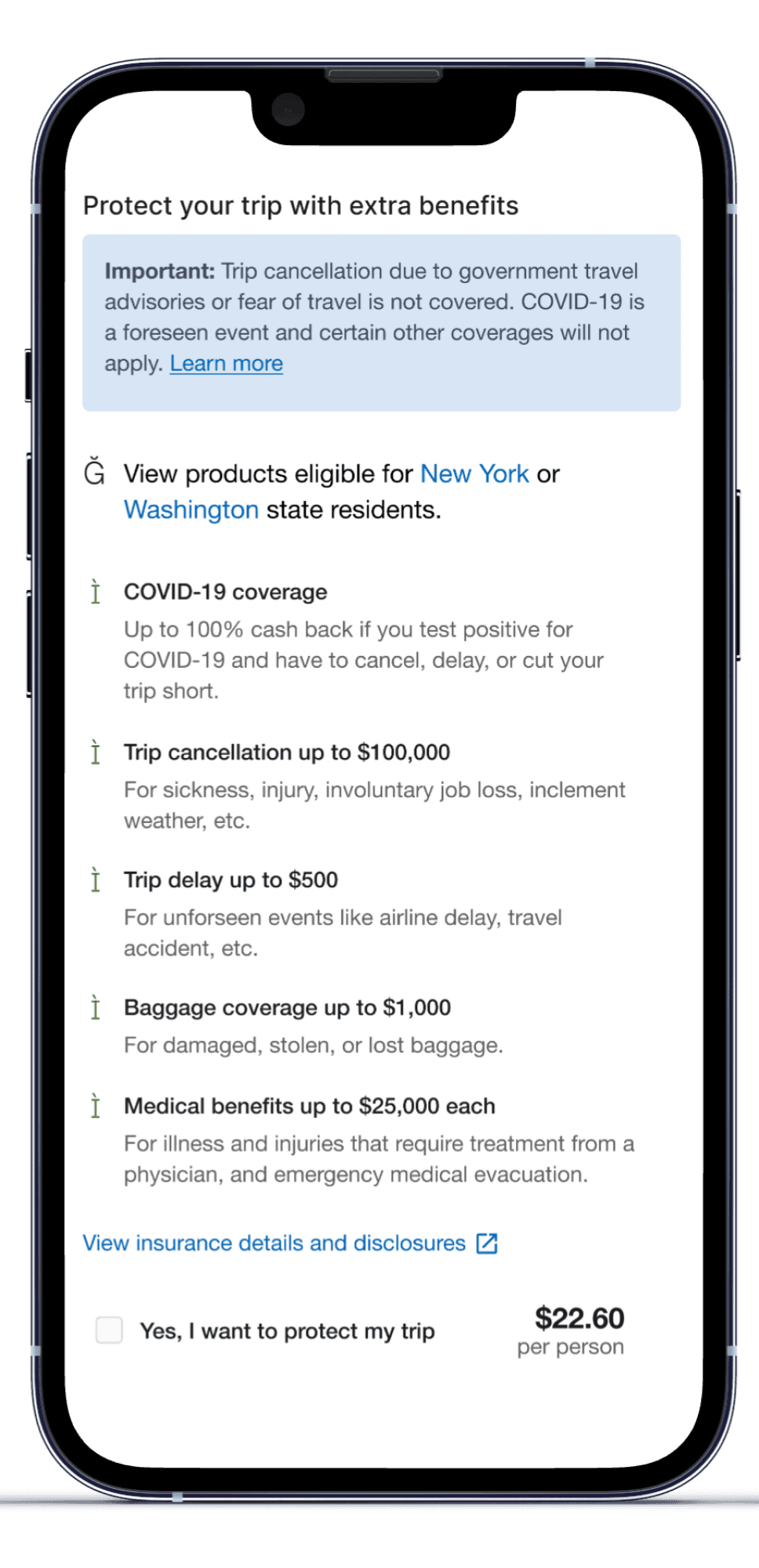

The Journey before CFAR

The workshop included the following:

Defining User Journeys

Value Proposition Mapping

Grouping Insights

Value Proposition Canvas

How Might We

Step 1

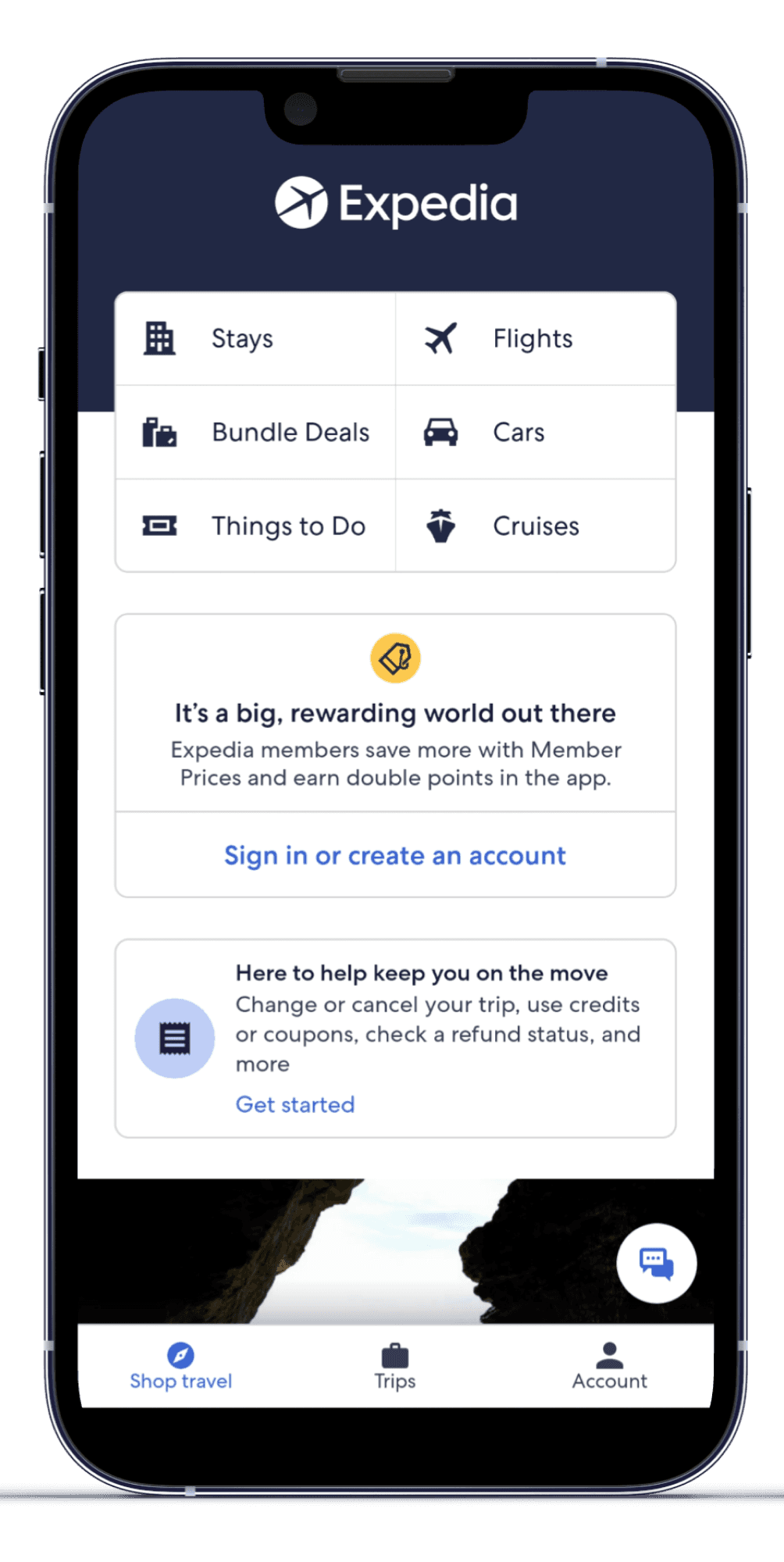

Home Page

This is where the user journey begins. The users decides the kind of trip they want to explore.

Impact?

Oh, we made some impact!

80%

Reduced claim processing time (From 2 weeks to 3 days)

$15M

CFAR specific revenue Generated in 2021-2022

8%

Percentage of trips booked with CFAR that were subsequently canceled

15%

From the pool of people who bought insurance

Performance Indicators

Key Learnings

We conducted a three-day research workshop for the product stakeholders to come together, understand the user problems, reframe the problem statement into achievable How-Might-We's, and run a robust feasibility analysis with the experts to find the best UX approach.

Cashback over Credits

We learnt that even the frequent fliers were deeply interested in cash-back over credits of any kind. they'd rather have their money in their hand, even though the credits could have been more value for money and hassle-free.

Users won’t pay more than 20%

As a matter of fact, we saw that user interest started declining substantially over the 17% premium mark and pretty much disappeared around the 20% premium mark on top of the base ticket price approached.

Future-proofing

COVID was a phase, and once it's gone, it might never return. We learnt that building the product so that it could merge seamlessly with the insurance product in the future without causing substantial user confusion was a great move.